Business add-backs

Know what to add back before valuing your business.

Add-backs are not extra profit.

They are adjustments to costs already included in the profit figure, so the business earnings can be looked at more cleanly.

The simple test is: was the cost already counted as an expense, and would it continue for a new owner?

If it was counted as an expense and would not continue, it may be an add-back. If the business still needs that cost, it should usually stay in the profit number.

Getting this right helps you avoid overstating or understating the profit a buyer is likely to look at. It also makes the conversation cleaner if you later decide to explore value, a sale, or a handover.

Owner pay is the part people most often get wrong.

The right treatment depends on the kind of business, the owner's role, and whether someone still needs to be paid to do that work.

In a smaller owner-run business, the owner may be the person doing the day-to-day work. If that wage is already counted as an expense and a new full-time owner could step into the role, it may be part of the owner-operator earnings.

In a larger or more managed business, the question is different. If the owner wage is higher than fair pay for the role, the adjustment is usually only the excess above fair pay.

Example: if the owner is paid $300k and fair pay for the role is $200k, the adjustment is $100k. If the owner is paid $300k and the role is not needed after sale, the adjustment may be the full $300k.

If you want the broader picture, the valuation guide explains how buyers think about business value.

Use the full owner pay only when it really becomes available to a new full-time owner-operator.

Use only the excess above fair pay when the role still needs to be paid properly after sale.

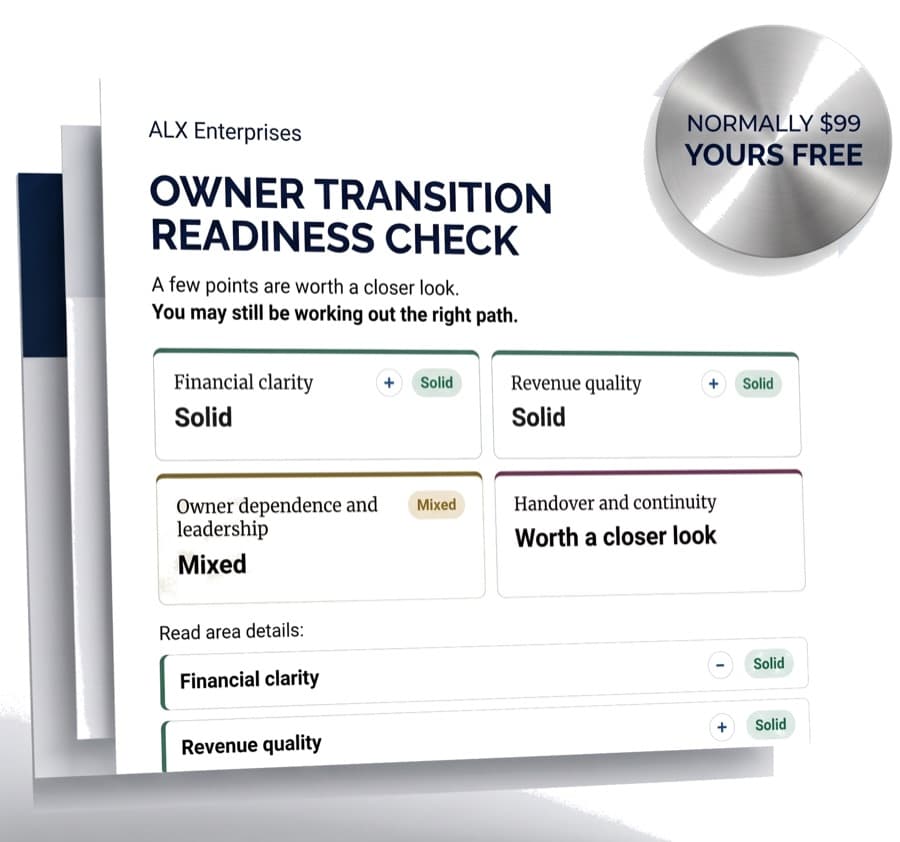

Find out how ready your business is for an ownership transition.

See what looks ready, what needs attention, and where to focus in under five minutes.

Some add-backs are more straightforward.

Interest, depreciation, and amortisation are often used to move from accounting profit toward a cleaner earnings number. The important thing is to use the same period as your profit figure.

Include it only if it is already included in the profit figure.

Include these when they are shown as expenses in the same accounts.

Use amounts from the same period as the profit number you entered.

Personal, family, and one-off costs need more judgement.

These can be legitimate, but they should be easy to explain. A buyer will usually want to know what the cost was, why it will not continue, and where it appears in the accounts.

If the cost sounds normal, recurring, or necessary for the business to keep operating, it probably should not be treated as an add-back.

Costs paid through the business that would not continue for a new owner.

Only the amount above fair pay for the role, not normal wages the business still needs.

Legal, professional, repair, or setup costs that are not expected to repeat.

Keep the number clean enough to be useful.

Add-backs do not need to be perfect at the first pass, but they should be simple, explainable, and tied to the same profit period.

Once you have a reasonable view of profit and add-backs, you can request a free valuation estimate as a simple next step.

Do not add back money that was never counted as an expense.

Do not add back wages or recurring costs the business still needs.

Do not add the full owner wage when only the excess above fair pay should be used.

Do not mix add-backs from a different period to the profit figure.

Claim your free valuation estimate.

Find out what your business could be worth.

Request a confidential estimate and replace the guessing with a clearer view of value, timing, and possible options to start building a sensible plan.

A few add-back questions owners usually ask.

These are the points that matter most before requesting an estimate.

What is an add-back?

An add-back is a cost already included in the profit figure that may not continue for a new owner. Adding it back helps show a cleaner view of maintainable earnings.

Should I add back my full wage?

Only sometimes. If you are the full-time owner-operator and a new owner could step into your role, the full wage may be relevant. If the role still needs to be paid at market rates, only the excess above fair pay should be considered.

Do drawings or dividends count?

Usually no. The simple rule is: only add back amounts that were already counted as expenses in the profit figure. If money was taken after profit, adding it back again would double count it.

What should I do if I am not sure?

Use rounded figures and stay conservative. A serious buyer conversation will test the numbers more carefully.